An Assurance Engagement Can Be Defined As

An audit to determine the validity of the subject matter. An engagement to enhance the reliability of the subject matter c.

2

2 An assurance engagement can be defined as.

An assurance engagement can be defined as. The objective of an assurance engagement is to obtain sufficient appropriate evidence to express a conclusion providing reasonable or limited assurance as to whether the audited body has complied with the specified requirements of the appropriate legislation the criteria in all material respects. The relevant quote from the Oxford online Dictionary defines an assurance as a positive declaration intended to give confidence. The sources of such criteria are least likely to include A.

Assurance engagement is an engagement performed by a practitioner to enable himself to express an opinion about the measurement of subject matter against a criteria. Best practices for another industry. An Auditor states an opinion as to whether the financial statements Give a true and fair view.

What is an assurance engagement. An engagement of an expert to direct the entity on subject matter. An assurance engagement can be defined as an.

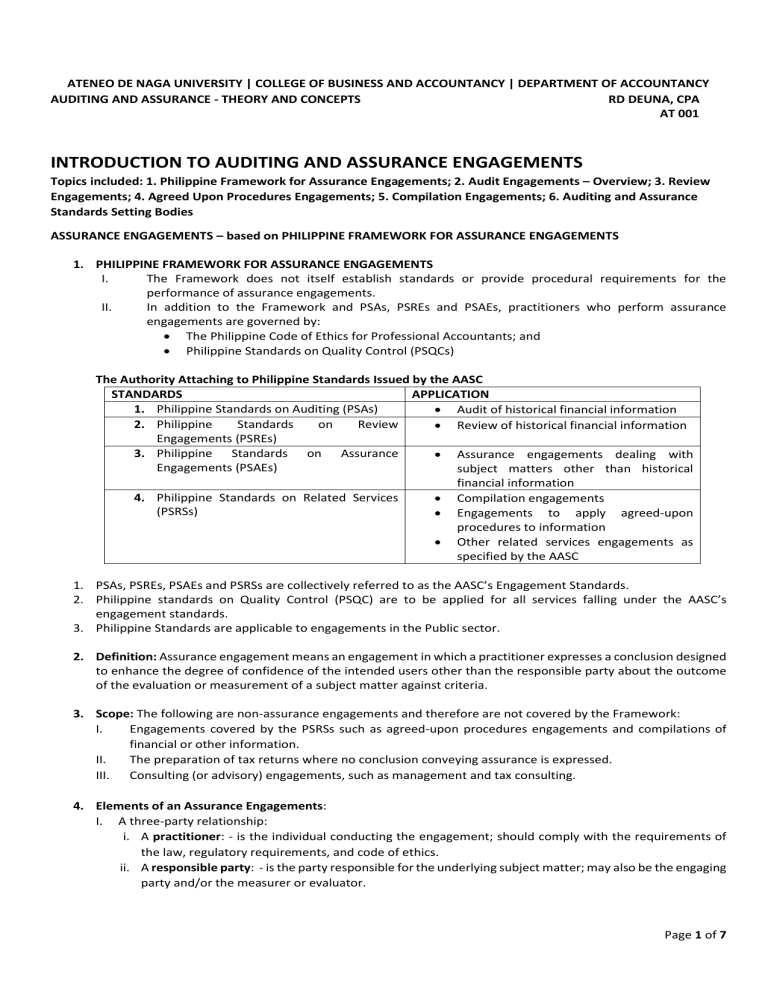

The terms of engagement in case of audit are in line with International auditing standards. An engagement to determine a true and fair view of the entities course of actions. The Philippine Framework for Assurance Engagements is not itself establish standards or provide procedural requirements for the performance of assurance engagements.

An appropriate subject matter is a identifiable and capable of consistent evaluation or measurement against the identified criteria. An engagement to enhance the reliability of the subject matter. For the purpose of Rule 2044 assurance engagement also includes a specified auditing procedures engagement as contemplated by the CPA Canada Handbook Assurance.

Audit engagement is for whole financial statements whereas certain assurance engagements can be for single financial statement out full set or specific element of financial statements or component or activities of the business. When an immediate family member of a member of the assurance team is a director an officer or an employee of the assurance client in a position to exert direct and significant influence over the subject matter information of the assurance engagement or was in such a position during the period covered by the engagement the threats to independence can only be reduced to an acceptable level by A. Government regulations for the industry.

An engagement to determine a true and fair view of the entities course of actions. The Audit and Risk Assurance Committee can therefore play a key role in seeking an optimum mix of assurance. A conclusion or opinion expressed in a written report appropriate to a reasonable assurance engagement or a limited assurance engagement.

Assurance services can include a review of any financial document or transaction such as a loan contract or financial website. An audit to determine the validity of the subject matter d. An assurance is not provided as the client determines the nature timing and extent of the evidence that is gathered.

The Three Lines of Defence model below can help in this respect. Before an assurance engagement can be performed the auditor must identify appropriate criteria. And b such that the information about it can be subjected to procedures for gathering sufficient appropriate evidence to support a reasonable assurance or limited assurance conclusion as.

An Auditor examines financial statements prepared by a board of directors to express an opinion as to whether they comply with accounting standards. ISQC 1 Paragraph 12q Relevant ethical requirements Ethical requirements to which the engagement team and engagement quality control reviewer. A promise From the same source engagement is defined as An arrangement to do something or go somewhere at a fixed time The auditor should be independent from the client company so that the audit opinion will.

To summarize the above formal definition read through the. An Assurance engagement in which the PractionerAuditor reduces engagement risk to an acceptably lower level in the circumstances of the engagement as the basis for the practitioners conclusion. The main objective of an assurance engagement is to let the professional and independent audit firms perform their works and express their opinion based on the level of assurance that they are engaging in.

Historical cost information for the processes examined. Benchmarks for the leading firms in the industry. INTERNATIONAL FRAMEWORK FOR ASSURANCE ENGAGEMENTS 5 FRAMEWORK FRAMEWORK This Framework calls these two types reasonable assurance engagements and limited assurance engagements2 Scope of the Framework.

23 There are different types of assurance that may have different strengths and may be best used in different ways. An engagement of an expert to direct the entity on subject matter b. This section distinguishes assurance engagements from other engagements such as consulting engagements.

An engagement to enhance the reliability of the subject matter b. When auditors are engaged in work where no assurance is provided this means. This review certifies the correctness and validity of the item.

An engagement to determine a true and fair view of the entities course of actions. Levels of assurance explained. Practitioners expression of opinion raise the confidence of the users over the measurement of subject matter subject to the criteria applicable under consideration.

Engagements and Section 291 IndependenceOther Assurance Engagements in Part B related to compilation engagements together with national requirements that are more restrictive. Start studying Exam 3 Chap 910121314 MCQ. Means an assurance engagement as contemplated in the CPA Canada Handbook Assurance.

An assurance engagement can be defined as. An assurance engagement can be defined as. An engagement of an expert to direct the entity on subject matter c.

The subject matter of an assurance engagement can take many forms. An engagement to enhance the reliability of the subject matter. An assurance engagement can be defined as a.

An audit to determine the validity of the subject matter d. Learn vocabulary terms and more with flashcards games and other study tools. The Philippine Framework for Assurance Engagements defines and describes the elements and objectives of an assurance engagement and identifies engagements to which PSAs PSREs and PSAEs apply.

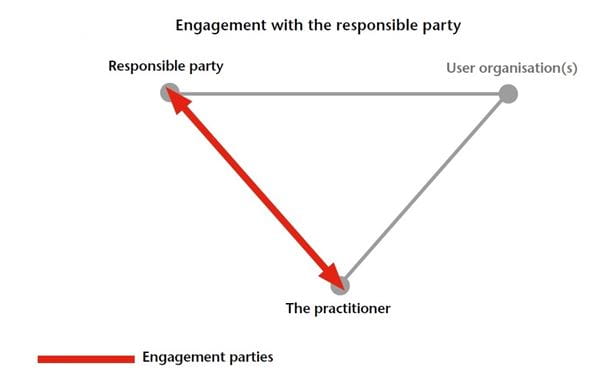

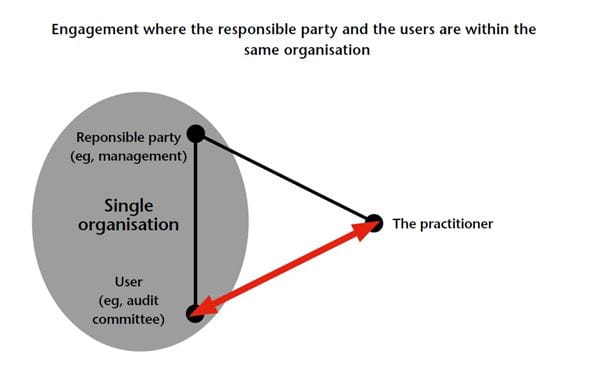

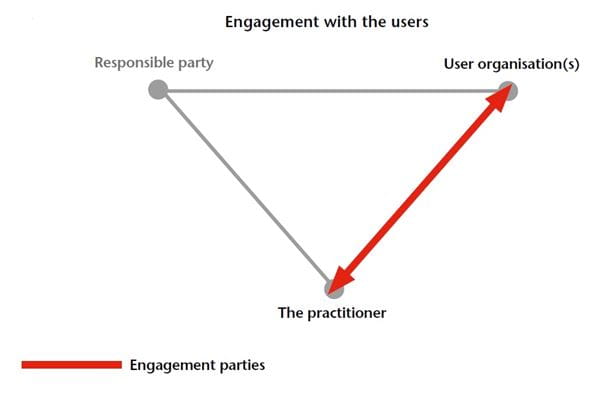

The need for assurance only arises when one party wishes to take comfort over a subject matter prepared by a second party and the assurance is only provided when a third party can provide an independent perspective. There are two common levels of assurance engagements that audit firms normally offer and provide.

Audit Engagement Letter

Chapter 1 What Is Assurance

Auditing Theory 250 Questions 2 With Answers 1 Accountancy Ac411 Studocu

Aut 001 Introduction To Auditing And Assurance Engagements

Assurance Service Engagement Ppt Download

Acca F8 Assurance Engagement Frameworks Relationships Youtube

Assurance Service Engagement Ppt Download

Assurance Service Engagement Ppt Download

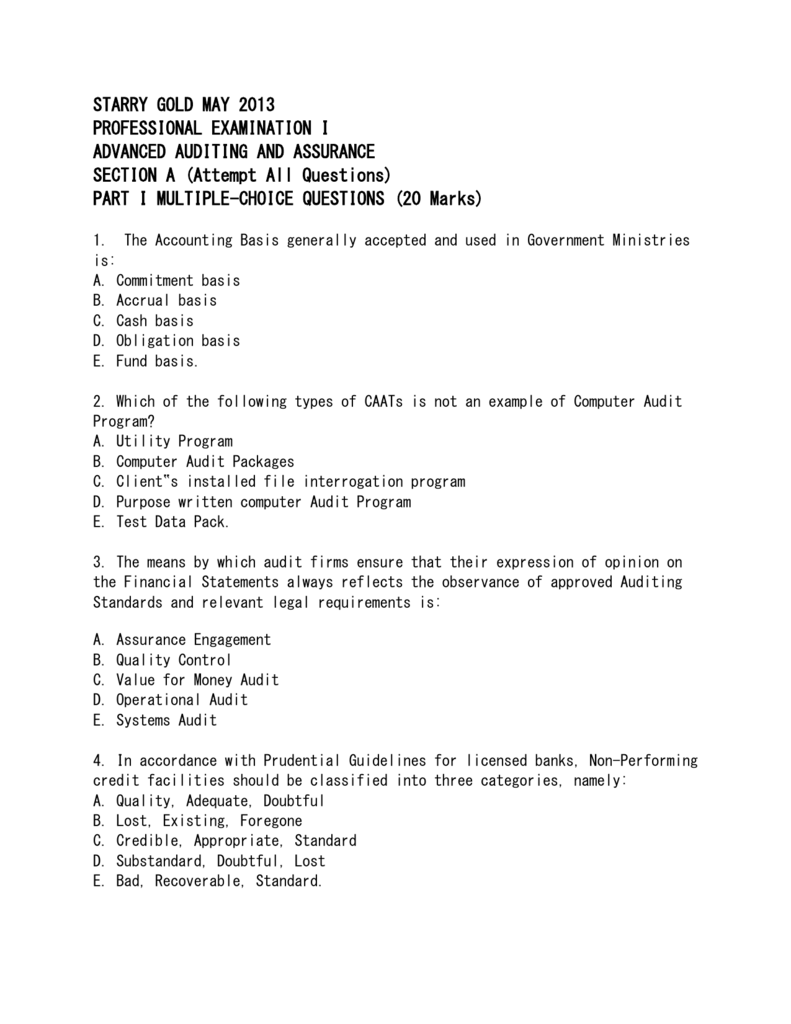

Part I Multiple Choice Questions 20 Marks

Three Party Relationship Assurance Process Icaew

Chapter 1 What Is Assurance

Assurance Service Engagement Ppt Download

Three Party Relationship Assurance Process Icaew

Extended External Reporting Assurance Current Practices And Challenges Krasodomska 2021 Journal Of International Financial Management Amp Accounting Wiley Online Library

Chapter 1 What Is Assurance

Chapter 1 What Is Assurance

Three Party Relationship Assurance Process Icaew

Chapter 1 What Is Assurance

Defining Attestation Auditing Assurance I S Partners Llc

Posting Komentar untuk "An Assurance Engagement Can Be Defined As"